The truth about that 3 digit number...

The importance of credit categories varies by person

Your FICO Scores are unique, just like you. They are calculated based on the five categories referenced above, but for some people, the importance of these categories can be different. For example, scores for people who have not been using credit long will be calculated differently than those with a longer credit history.

In addition, as the information in your credit report changes, so does the evaluation of these factors in determining your FICO Scores.

Your credit report and FICO Scores evolve frequently. Because of this, it's not possible to measure the exact impact of a single factor in how your FICO Score is calculated without looking at your entire report. Even the levels of importance shown in the FICO Scores chart above are for the general population and may be different for different credit profiles.

Your FICO Scores only look at information in your credit report

Your FICO Score is calculated only from the information in your credit report. However, lenders may look at many things when making a credit decision, such as your income, how long you have worked at your current job, and the kind of credit you are requesting.

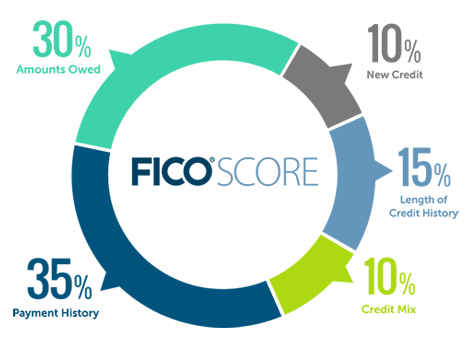

What categories are considered when calculating my FICO Score?

Payment history (35%)

The first thing any lender wants to know is whether you've paid past credit accounts on time. This helps a lender figure out the amount of risk it will take on when extending credit. This is the most important factor in a FICO Score.

Be sure to keep your accounts in good standing to build a healthy history.

Amounts owed (30%)

Having credit accounts and owing money on them does not necessarily mean you are a high-risk borrower with a low FICO Score. However, if you are using a lot of your available credit, this may indicate that you are overextended—and banks can interpret this to mean that you are at a higher risk of defaulting.

Length of credit history (15%)

In general, a longer credit history will increase your FICO Scores. However, even people who haven't been using credit for long may have high FICO Scores, depending on how the rest of their credit report looks.

Your FICO Scores take into account:

How long your credit accounts have been established, including the age of your oldest account, the age of your newest account and an average age of all your accounts

How long specific credit accounts have been established

How long it has been since you used certain accounts

Credit mix (10%)

FICO Scores will consider your mix of credit cards, retail accounts, installment loans, finance company accounts and mortgage loans. Don't worry, it's not necessary to have one of each.

New credit (10%)

Research shows that opening several credit accounts in a short amount of time represents a greater risk—especially for people who don't have a long credit history. If you can avoid it, try not to open too many accounts too rapidly.